Blog

This month, Ethiopia’s new Investment Tax and Customs Duty Incentive Regulation (No. 586/2026) governing tax incentives for investors has come into effect. The key changes are:

Under the previous investment incentive regulation, eligible investors could obtain business income tax holidays (exemptions) for 1 to 5 years for most investment activities in Addis Ababa and Oromia Shaggar Zone, and 2 to 6 years elsewhere. Forestry and related activities enjoyed 8 to 9 years of income tax exemptions, while the development and rental of Special Economic Zones (SEZs) enjoyed 10 years of income tax exemptions in Addis Ababa and the Oromia Shaggar Zone and 15 years elsewhere.

The new regulation replaces income tax holidays with temporarily reduced income tax rates. For a limited period, qualifying investors enjoy a reduced business income tax rate below the standard rates of 30% for incorporated businesses and 35% (top marginal tax rate) for sole proprietors. The Minimum Alternative Tax (MAT), which is usually payable at a rate of 2.5% of turnover if business income tax payable falls below that level, is reduced proportionally to the reduction in the business income tax rate. [1]

As under the tax holiday scheme, existing companies seeking to benefit from investment incentives need to prepare separate accounts between their existing business and the new investment; only profits relating to the new investment benefit from the reduced income tax rate.

In addition to these investment incentives in a strict sense, reduced income tax rates are also available for businesses engaging in certain activities:

Unlike the previous regulation, the new regulation no longer allows loss carry-forward from the incentive period to later years. Compared to the previous regulation, the sectoral coverage of the scheme is significantly narrower; at the same time, some reasons for incentives such as listing shares or environmental protection activities have been added. Overall, the changes amount to a substantial reduction in the generosity of the tax holiday scheme.

Beyond a desire to cut the cost of the tax holiday scheme, the switch to a 15% reduced rate for most beneficiaries was largely motivated by the Global Minimum Tax implemented through the GloBE rules (Pillar II). Under the GloBE rules, multinational firms that pay less than 15% tax on their income under the GloBE definition can be charged top-up taxes in other jurisdictions on their Ethiopia-derived income. This could have prevented multinational firms from benefitting fully from tax holidays and might have led to revenue leakage from Ethiopia to other jurisdictions.

The reform also addresses some long-standing concerns about tax holidays as a policy tool. One is that investors could previously avoid paying income tax on their established businesses by shifting profits towards business activities qualifying for tax holidays (Clark and Skrok, 2019). Another is that investors might have closed businesses when tax holidays expired just to open new businesses to benefit from the tax holiday again. A third is that tax holidays produce the biggest tax savings for projects that are highly profitable, which would usually have gone ahead even in the absence of the tax holiday. None of these issues are fully addressed by the new regulation, but they are substantially ameliorated by the lower generosity of the scheme.

Another key feature of the new investment incentive regulation is the introduction of performance requirements for retaining incentives. Eligible investors are required to sign a performance agreement with the relevant government institution, which for most investments is the federal or regional investment institution. This agreement will contain specific and measurable commitments regarding sector, capital invested, employment generation, production capacity, and contributions to technology transfer. The investment institutions will report any breaches of the agreed-upon performance indicators to the Ministry of Finance, which can then revoke or suspend investment incentives.

These performance targets are aimed at ensuring better value for money for the investment incentives scheme. A widespread concern about the existing scheme was the absence of a robust system of monitoring investment tax incentives. Policy makers were concerned that this created accountability gaps for both investors and government/regulatory institutions, undermining the effectiveness of the incentives in attracting investment, creating jobs, and promoting economic growth.

However, it is not clear how effective performance agreements will be in addressing this issue. As it stands, there is no clear guidance regarding what quantities of capital invested, jobs created, etc. should be expected form investors. This raises the possibility that some investors will submit unreasonably low targets, which civil servants might find difficult to identify. Discretion over whether to apply a sanction if performance targets are not met, while enabling civil servants to take account of extenuating circumstances, might also lead to uneven enforcement across businesses. The operation of this system should be subject to review and evaluation to ensure enforcement is appropriately fair and robust.

A third key change in the new investment incentives regulation is the introduction of a first-year investment allowance, which offers accelerated depreciation for large investments. Firms investing at least USD 2 million or its equivalent in ETB in selected capital goods – factory buildings, manufacturing machinery, mining equipment, and agricultural mechanization equipment – can deduct 50% of the cost of the capital good in the year of purchase. The remaining 50% are deducted over the next two years at 25% each year.[4]

It is not clear how popular this scheme will be with investors. On the one hand, high inflation in Ethiopia makes accelerated depreciation especially attractive, as tax liabilities are shifted to future tax years when they will be worth substantially less in real terms. On the other hand, as the MAT creates additional tax liabilities for loss-making firms, loss carry-forward is limited to five years in Ethiopia, and many investors are eligible for temporarily lower tax rates in the period after making an investment (see above), many investors would actually end up paying more tax if they made use of the investment allowance. As a result, take-up of the scheme is likely going to be limited to large investors that have high profits from existing activities and that are ineligible for a temporarily reduced income tax rate – potentially quite a small set of firms.

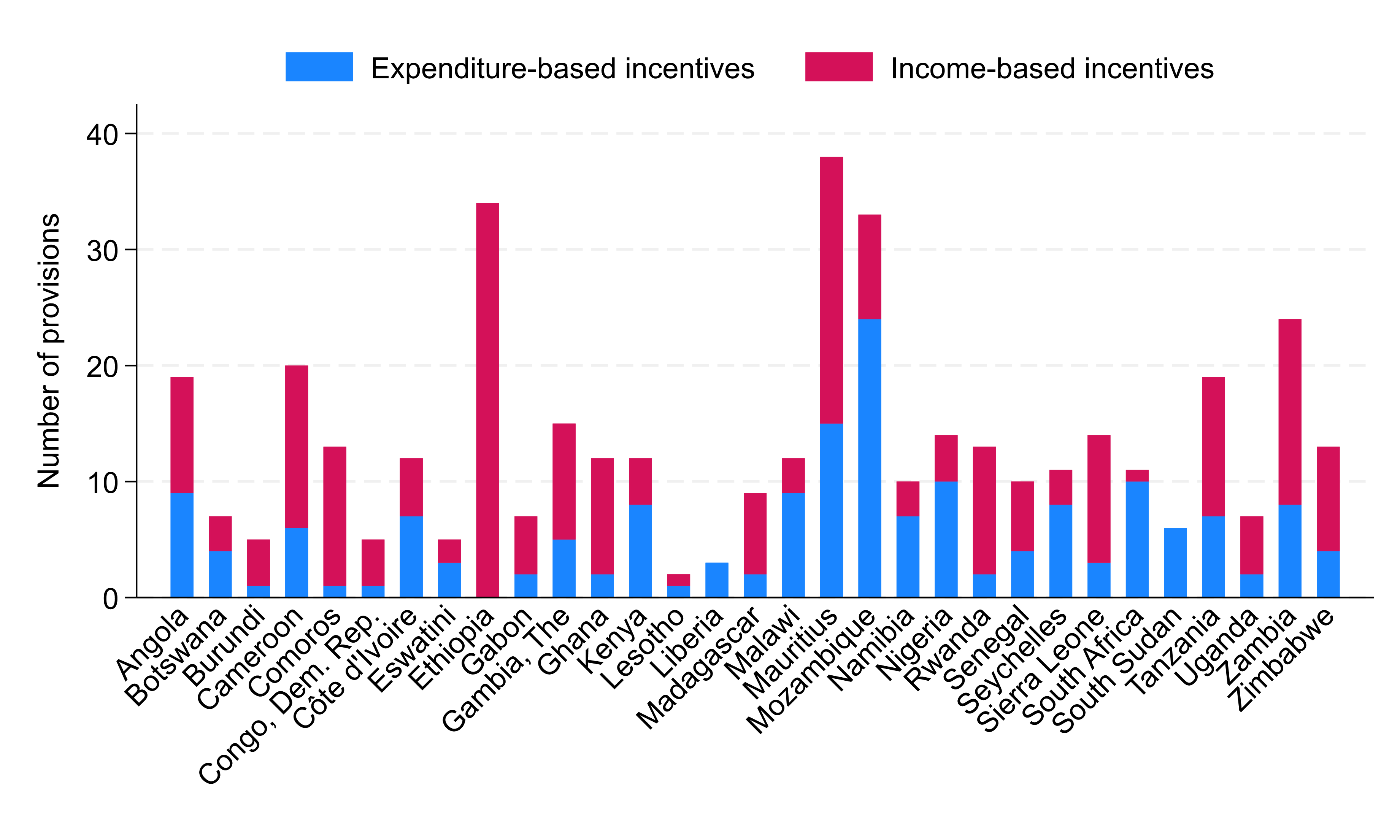

Nonetheless, the introduction of the investment allowance is significant because it could be a first step towards more expenditure-based incentives (also known as cost-based incentives). As shown in the chart below, introducing an expenditure-based incentive brings Ethiopia into line with other countries in the region. According to the OECD Investment Tax Incentive Database, all other countries in sub-Saharan Africa have at least one expenditure-based incentive; Ethiopia was previously the only country to rely purely on profit-based incentives (namely, tax holidays). While profit-based incentives can have a useful role in attracting ‘footloose investment’, it has become conventional wisdom that expenditure-based incentives tend to be more cost-effective overall (OECD, n.d). This is because expenditure-based incentives lower the cost of investments directly, while profit-based incentives only lower it indirectly through the taxation of future profits (see e.g. OECD, 2025).

Tax incentive types for sub-Saharan African countries in 2024

Source: authors’ calculation based on the OECD Investment Tax Incentive Database

Ethiopia’s new investment incentive regulation aims to rationalise incentives while preserving the broad outlines of the existing system. Transforming the tax holiday scheme into a scheme offering temporarily reduced tax rates and narrowing its sectoral coverage should reduce forgone revenue substantially. The introduction of performance agreements has the potential of improving value for money, but much will depend on how effectively they are used. The introduction of a first-year investment allowance is a first step towards a more modern system of investment tax incentives, moving Ethiopia towards international best practice in this area.

[1] In each case, the benchmark is the standard business income tax rate for incorporated businesses (30%). For example, if a business benefits from a reduced income tax rate of 15%, its MAT rate will be reduced to 1.25% regardless of legal form. ↩

[2] The Regulation gives the Ministry of Finance the power to issue a Directive granting further income tax incentives (limited to an extension of the duration) for investments in remote areas. ↩

[3] The details will be set out in a directive to be issued by the Ministry, which will outline the implementation process for this provision. ↩

[4] Note that exactly 100% of the investment cost (in nominal terms) can ultimately be deducted, which makes this type of incentive unproblematic under the GloBE rules. (In UK terminology, the scheme is akin to ‘(enhanced) first-year allowances’ and not ‘initial allowances’.) ↩

OECD. (2025). Corporate Tax Statistics 2025. OECD Publishing. https://www.oecd.org/content/dam/oecd/en/publications/reports/2025/11/corporate-tax-statistics-2025_09806d11/6a915941-en.pdf

Clark, W. S., & Skrok, E. (2019). The use of corporate tax incentives: A guidance note and experience from Poland, Hungary and Latvia. World Bank Group. https://documents.worldbank.org/en/publication/documents-reports/documentdetail/180801564468287868

OECD. (n.d.). Investment incentives, promotion and facilitation. Organisation for Economic Co operation and Development. Retrieved January 26, 2026, from https://www.oecd.org/en/topics/sub-issues/investment-incentives-promotion-and-facilitation.html

Published on: 17th March 2026

Print